STRUGGLING With Stubborn Fat That Won’t Disappear? No Matter Your Age, No Matter What You Try...

It’s Still There…!

Absolutely Free Training Video

Reveals

The Game-Changing Secret To Vaporize Fat Cells!

Click the button below now, to Watch your Absolutely Free Training Video before it’s gone!

=> Yes ! Watch My Free Video Now !

Larry Humphreys, a retired Federal Emergency Management Agency worker in Moultrie, Georgia, says he and his wife won’t be traveling much next year when their monthly health insurance premiums rise more than 40 percent to $938.

Humphreys, 68, feels betrayed by the federal employee health benefits program. “As federal employees, we sacrificed good salaries in the private sector because we thought government benefits would be better now, in retirement,” he said.

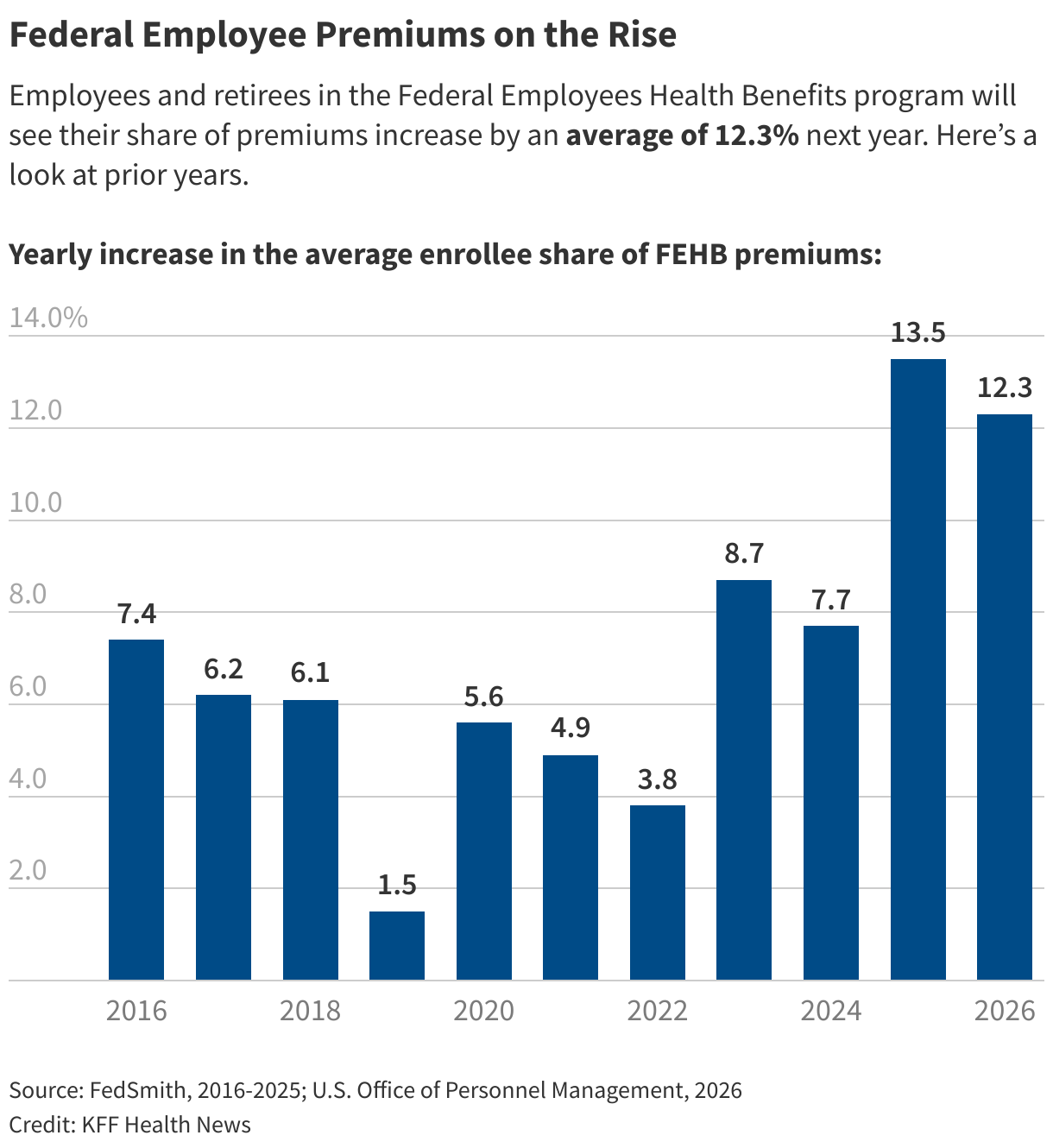

As the nation’s largest employer-sponsored health insurance program, the FEHB program covers more than 8.2 million federal government employees and retirees and was once celebrated as a national model for controlling costs while giving enrollees many health plan options.

But next year, the system’s average enrollee premiums are set to jump more than 12 percent, on top of a 13.5 percent increase in 2025. The two-year increase is greater than that of many private employers and their employees.

FEHB’s rate hikes are similar to plans sold on the Affordable Care Act exchanges — without government subsidies for most enrollees, a major point of contention on Capitol Hill. Insurance companies charge an average of 26 percent for Obamacare plans in 2026, after a 4 percent increase this year.

The timing of the latest FEHB rate hike is even harder for millions of federal workers to stomach: The 2026 increase was announced in October, when many federal workers were on unpaid leave during a 43-day government shutdown.

Unlike most private employers, the FEHB program offers enrollees numerous health plans to choose from. This allows some people to lower their monthly payments by switching to plans with higher deductibles or payments. But each year, only about 5% of enrollees switch plans, according to the human resources office that oversees the program.

Humphreys, who has stayed with the same health plan for decades despite consistently higher prices, said it’s difficult to determine which plan is best based on their health status. He has glaucoma and diabetes, and his wife Julianne has suffered from heart problems.

Their FEHB plan covers the costs of their care not covered by Medicare, which typically pays 80 percent of their health bills.

“There’s a fear that if you do something and change plans and it’s wrong, you might be in a bad place,” he said.

Open enrollment for federal employees and retirees runs through December 8.

According to OPM, factors driving the increase in premiums include an aging federal workforce with more chronic conditions and the use of prescription drugs, including expensive GLP-1 drugs for weight loss.

About 42 percent of federal workers are over age 50, compared to 33 percent in the general workforce, OPM says. About 7 percent of federal workers are under the age of 30, compared to about 20 percent of workers.

OPM officials said the Trump administration’s policy to lower drug costs, which focuses on preventing expensive medical conditions, will hopefully help it control premiums in the future.

“Of course, none of these initiatives will happen overnight — turning the $79 billion ship around is slow and steady,” Shane Stevens, OPM’s deputy director for health and insurance, said in a news release. “But we are committed to improving the quality of life and quality of care for our members while ensuring that health care remains accessible and affordable for those who work (or have worked) for the American people.”

OPM did not respond to requests for comment.

John Holahan, a health policy fellow at the nonpartisan Urban Institute, said OPM’s explanation left out a key reason for rising premiums: hospital consolidation. Although the FEHB program is a collection of health plans, in many markets—including the Washington, D.C., area—those insurers must negotiate with a handful of high-performing health systems that have bought other hospitals and doctors. That market power allows them to push prices higher on FEHB plans, he said.

Jacqueline D. Bowens, president and CEO of the DC Hospital Association, said in a statement that “the costs patients pay are determined not only by the care they receive, but by how insurance companies decide to price, reimburse and limit access to care.”

Holahan said it’s surprising that FEHB premiums are rising even faster than other, smaller employers. But he’s not surprised that federal employees don’t switch plans more often, even if it’s in their financial best interest.

“People think the world of health care is so complicated,” he said. Holahan, a noted health economist, said he, too, finds it scary to switch Medicare health plans.

Mike Lindquist, chief scientific review officer at the National Institutes of Health, said he is not happy with the increase in his fees over the past two years. “It’s difficult because it’s a big expense.”

Lindquist, 43, who lives in Brunswick, Maryland, has been on the same Blue Cross and Blue Shield plan through the FEHB program for the past few years, though she evaluates her options every fall.

“If you don’t switch, you don’t have to worry about choosing a new plan that may not be right for your carrier,” he said.

Jonathan Foley, a health consultant who served as a senior adviser to OPM during the Biden administration, said the premium increases will be a hardship for many enrollees. Although the FEHB program offers a total of 200 health plans, about 10 to 20 in each geographic market, enrollment is concentrated in only a handful of Blue Cross and Blue Shield plans.

“This concentration reduces competition and gives leverage” to Blue Cross and Blue Shield rate hikes, Foley said in an email.

He said the FEHB program also has higher costs because its health plans cover GLP-1 drugs like Wegovy and Ozempic. Nationally, less than half of large employers offer this benefit, according to the Peterson Center on Healthcare and KFF. KFF is a health information organization that includes KFF Health News.

Another cost pressure has been more members using behavioral health benefits to treat depression and anxiety since the start of the Covid pandemic, Foley said.

Cuts to the Trump administration’s federal workforce have also contributed to increased costs, Foley said. OPM has lost about a third of its employees in the past year, leaving fewer workers overseeing the FEHB program and negotiating with dozens of health insurance companies, he said.

“Workforce reductions and the unpredictable nature of policy under the Trump administration have created considerable uncertainty among health insurers,” Foley said. “Actuaries’ response to increased uncertainty is to raise interest rates.”

A report this year by the Government Accountability Office noted that recent OPM staff vacancies led to the suspension of fraud risk assessments in the FEHB program.

John Hatton, vice president of policy and programs for the National Active and Retired Federal Employees Association, an advocacy group, said the higher rates mean it’s important for FEHB members to shop around and compare plans for next year. “The program is designed to promote competition to mitigate and reduce costs,” he said.

Hatton said OPM research shows the top reasons people don’t change their plans are choice and worry about making a mistake. Switching to a plan with even a slightly higher deductible could save people a few hundred dollars a month in premiums, he said.

But Humphreys, a Georgia retiree, said he likes that his current plan keeps him and his wife low. They owed a little money when his wife contracted kidney stones and sepsis, which put her in the hospital for 12 days.

That assurance will soon become more expensive: Their FEHB and Medicare payments will take up more than half of his retirement check next year after taxes.

“I can take a lower premium plan, but that’s a gamble I’m not willing to take,” he said.